What is an Annuity Payment And How Does It Work?

4 min read

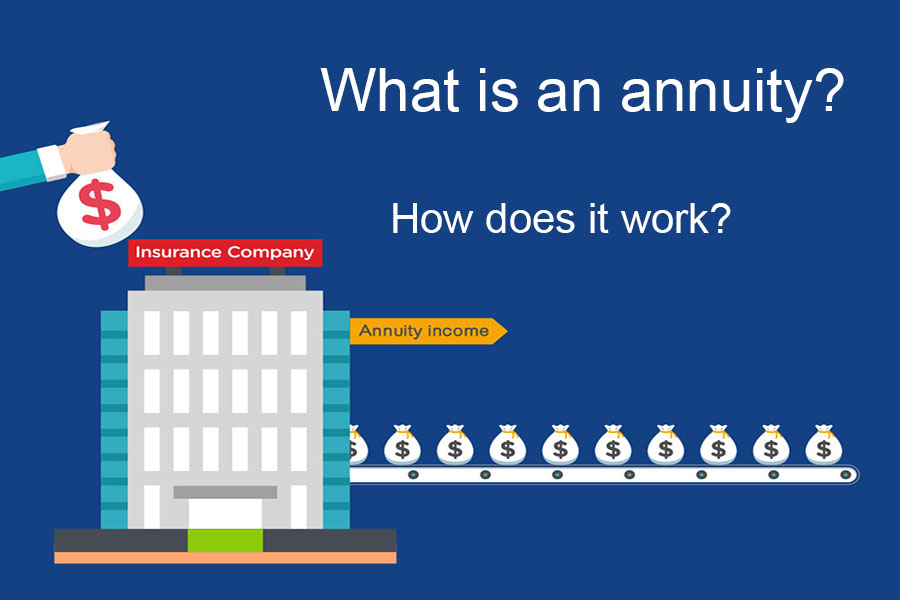

An annuity is a long-term investment plan offered by insurance companies and other financial institutions where you have to put a specific sum of money at a time or over some time. As an investor, you are entitled to receive regular payment after a certain time. The payout can also be lump-sum instead of periodic payments. An annuity plan is a negotiable financial instrument that can be sold in the secondary market before its maturity.

For example, Mr. X is 30 years old now. He bought an annuity plan from Y company Ltd. At a lump-sum amount of Z. As per the plan, Mr. X is entitled to receive XY amount per month when he will turn 60 years of age. The annuity payout will continue for 30 years.

Many people invest in an annuity for a safe and steady income stream to support their living during retirement.

Type of Annuity

Immediate Annuity: – In an immediate annuity plan, there is no cool-down period as such. The annuitant invests lump-sum money and starts receiving the payout from the immediate next payment cycle. The annuity could be lifelong or for a certain period. This sort of annuity plan is suitable for those who received a large sum of money at a time maybe by selling a property or, winning a lottery or, gaining a profit from speculative investment.

Deferred Annuity: – Deferred annuity is similar to the concept of pension where the investor invests money during the accumulation period and starts receiving the payout in their vesting period. The vesting period is most likely to start after the retirement of the investor. A deferred annuity gives the annuitant financial security he needs at his old age.

Periodic Annuity: – In a periodic annuity, the investor receives a payout each time after a certain interval which could be either monthly, quarterly, or annually. It is the opposite of the concept of the lump-sum annuity.

Lumpsum Annuity: – In a lump-sum annuity plan, the annuitant is entitled to receive his/her payout as a lump-sum amount although the investment could be done in a lump-sum or periodic manner. It is just the other way around of the periodic annuity concept.

Variable Annuity: – Variable annuities are market-linked annuity plans which give higher return if the insurance company makes a higher profit. The opposite happens when the market faces turmoil. Therefore, this type of annuity doesn’t give a guaranteed payout during the vesting period.

Fixed Annuity: – In a fixed annuity plan, the payment will be consistent over the entire payout period. The fluctuation in the market condition will not hamper the assured amount of payout that the annuitant is entitled to receive. Therefore, it is considered to be an ideal post-retirement pension plan.

How Does Annuity Work?

Wondering how the entire system of annuities works? Well, here is how it does.

– The investor invests a lump-sum or series of installments into an annuity plan offered by financial institutions like banks, insurance companies, etc. to enjoy the future benefits of an annuity.

– The annuity payment starts being paid out to the beneficiary after an agreed period. The Recipient may receive the payout at an equal interval or, as a one-off payment depending on the structure of payout within the plan.

– The investor has also the option to sell the annuity on a secondary market annuity for immediate cashout.

– The Annuitant has the right to determine whether he/she wants the payout periodically or, lump-sum. It depends on the individual’s needs. He may choose to receive a monthly payment for the rest of his life which will secure a steady income for a living when he/she will go to retirement.

– The payout may also vary depending on the length of the time investor wants the regular payment for. For example, an investor may choose to receive an annuity payout for 30 years after a certain time whereas another investor may choose to receive the payout for 15 years. If both of them has invested an equal amount of money for an equal length of accumulating period, they are going to receive different amount of annuity payout. The investor with 15 years payout will receive more money in each payment cycle than that of the one who chooses to receive a payout over 30 years.

– The investor also has options to opt for a fixed annuity or, performance-based annuity. In the case of a fixed annuity, the payout amount is guaranteed whereas, in the case of the performance-based payout, the actual figures that the investor will receive depend on the output the company or, market has produced.

Although annuity is an insurance product many large and small companies offer annuity plans e.g., banks, insurance companies, independent brokers, and other financial institutions. The type of annuity to buy depends upon your future need and current financial position. Therefore, it is highly advisable to do your research before investing in an annuity product.